This spring, more than 6,100 students at more than 170 institutions completed the Graduating Student Questionnaire (GSQ), which is administered annually by the Association of Theological Schools (ATS). The GSQ asks new graduates about their demographic information, vocational goals after graduation, and perceptions of the effectiveness of their theological education. During the last year, in conjunction with a grant from Lilly Endowment Inc. to coordinate a project focusing on the Economic Crisis Facing Future Ministers (ECFFM), ATS has been carefully analyzing student debt among graduates.

|

Insights

Through the GSQ data and reports from the 67 institutions participating in the ECFFM initiative, we are finding that student debt varies greatly among our students and from institution to institution. Among those students who complete the GSQ, some of the trends are especially noteworthy:

-

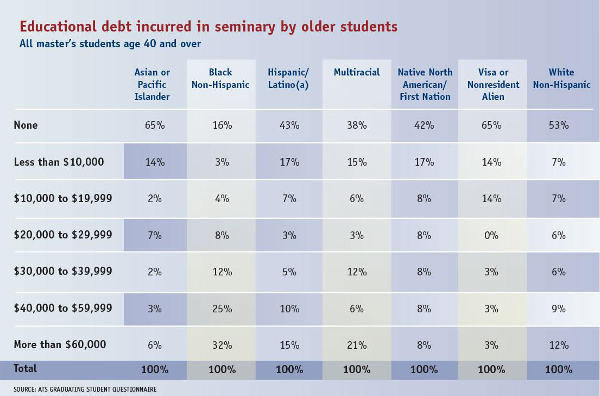

While older students generally bring less debt with them as they start their theological studies, during the course of their program they seem to be incurring just as much debt as younger students.

-

Student debt varies significantly by race/ethnicity, with black students, especially older black students, incurring far more debt than students of other races and ethnicities.

-

Single students are slightly more likely to incur higher levels of debt than are married students. Single female students take on more debt than single male students.

|

Analysis

Student debt varies greatly from institution to institution based on a variety of factors — tuition costs, cost of living, scholarship distribution practices, and more. It is important for each school to have an accurate picture of how much educational debt its students are incurring, and which students are taking on the highest amounts.

Debt among older students is a particular concern not just in theological education, but in higher education as a whole. In a recent article on Time’s Money page (time.com/money/3913676/ student-debt-into-retirement), Michaela Ross provides insights from consumer rights attorneys who have observed that older students often see education “as a pathway out of poverty and toward financial stability, but the reality is much different from that.” Older students have fewer years of earning capacity and, if older students default on their student loans, the federal government can garnish their Social Security benefits.

In theological education, debt among older students is significant, because seminary graduates are less likely to take high-paying positions after graduation, thus decreasing their ability to repay loans. There has been a dramatic increase in the number of older students enrolling in seminary in the last decade, so the collective student debt among these students is likely to grow over the coming years.

Given the large number of women seminarians, and the increasing racial and ethnic diversity among theological schools in the United States and Canada, it’s worth taking gender and ethnicity/race into account when examining student debt. When we study student debt, we should not assume that it is a merely individual issue — that the only students who take on high levels of debt are those who are irresponsible or not good with money. Data on black student debt in particular highlights the way that debt can be a systemic issue facing an entire community of students. Such systemic issues of debt point to larger economic issues connected with the histories of race within the broader culture and within the church.

|

Next steps

When it comes to student debt, it’s important to know your students. Using the GSQ or some other method, faculty and boards should be made aware of how much debt students are taking on during their seminary years — and, in at least a general way, which students are most affected.

Anthony T. Ruger, a longtime consultant on seminary finances, recommends that schools create a bar graph illustrating the cumulative debt level for each student, marking how much debt was brought into the seminary and how much is being incurred while the student is enrolled. Some institutions also try to gather data on non-educational debt, such as credit card bills and personal loans. Such graphs can help institutional leaders better understand the distribution of debt among the student body.

Once you have a general sense of the amount of debt your new graduates are carrying, you can compare your data to trends in theological education. Information on debt among graduates of ATS schools can be found in the Total School Profile posted on the ATS website. See www.ats.edu/resources/student-data/archived-student-data-reports.

With student debt, however, context is important. Institutions should gather information on the average starting salary of their graduates — information that helps determine what amount of student loan payments might be manageable. Starting salaries vary by denomination and by the types of positions that students are offered upon graduation. But starting salaries can also vary by the missional focus of the institution. Schools that focus on preparing bivocational pastors, social justice ministers, or pastors for underserved constituencies may conclude that reducing student debt is critical if the school is to pursue its mission.

It’s important to dig deep into the data at your own institution. Are there certain groups that are incurring more debt than others? Certain students who are graduating debt free? Are debt levels in your institution affected by age, gender, or race/ethnicity? How is student debt affected by your scholarship distributions? In some institutions, a majority of scholarship aid goes to full-time, denominationally affiliated M.Div. students — those that were traditionally considered to be “most promising.” But if most debt is being accrued by single women older than 40, it may be time to rethink traditional scholarship priorities.

Once you have a sense of the shape of student debt among your student body, you can begin to design a strategy that fits both your students and your institution. You might consider financial literacy training for students, changes to curriculum, innovative funding strategies, or creative ways to lower the cost of theological education.

But whatever strategies you choose must be owned by the institution as a whole, including boards, administrators, faculty, and students. That’s why it’s important to share the data widely and graciously, recognizing that educational debt is rarely an individual issue. Instead, it is part of the larger economic issues facing churches, theological schools, communities, and the culture at large.

And share the data with hope, believing that change is possible.

The figures in this article are from the 2014–15 Graduating Student Questionnaire (GSQ)’s Total School Profile, which is issued by the Association of Theological Schools. More information: www.ats.edu/resources/student-data.

Additional resources to help institutions respond to student debt, including relevant research studies, strategies to reduce student debt, and financial literacy resources (including course syllabi) can be found on the ECFFM resource page at www.ats.edu/resources/current-initiatives/economic-challenges-facing-future-ministers.