Seminaries exist to prepare students for ministry, service, and scholarship that benefits the church and the wider world, but the current student debt crisis is severely hindering this critical mission.

First, high levels of personal and academic debt discourage students from applying to theological schools in the first place. And second, many seminary graduates end up carrying a debt burden that is so overwhelming it derails them from taking lower-paying jobs in the church, academia, and the nonprofit sector, pushing them away from positions in ministry and service.

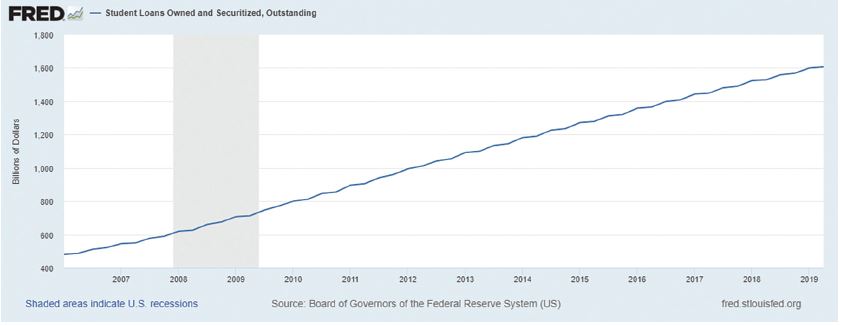

Shortly before 2008, the overall student loan burden in the United States stood at under $500 billion. After the Great Recession that started that year, loan balances across the board (including mortgages, car loans, credit cards) decreased sharply as debt was paid down or eliminated by insolvency and bankruptcy. However, as the chart on the previous page shows, education debt continued to increase without so much as a blip. By 2018, 69 percent of undergraduate students had student loans, and their average debt was nearly $30,000. Moreover, in 2018, more than 11 percent of student loan debt was at least 90 days delinquent.

In 2019, total student loan balances in the United States rose to their highest rate ever. More than $1.5 trillion is now collectively owed by 44.7 million people from all demographics and age groups. And this does not include consumer debt like credit card loans and car loans.

How is the student loan problem affecting seminaries and seminarians?

Student loan debt is keeping people out of seminary

I have spent many years providing financial planning services to families. People who consult a financial planner when their children are young usually have two primary goals: to retire comfortably and to save enough to pay for their children’s undergraduate college tuition. Paying for their children’s graduate school tuition, however, is a different story — most parents do not feel obliged to plan at all for supporting their children’s graduate education, especially when we project the eye-popping price of an undergraduate education.

Undergraduate costs are so exorbitant that when the time comes, many parents take out loans or adjust their retirement savings goals to pay for their children’s tuition and other costs. As a result, providing funds for graduate school, including seminary, is out of the question for most parents.

But what about the students themselves? Many students are open to taking on significant levels of debt to pay for graduate school because of the income potential offered by a graduate degree. But while student loans may be a good investment for graduates who are entering high-income professions, the income potential for graduates of theological schools is relatively low.

This problem of student debt is compounded by the finances of theological schools. Over the past 20 years, church and denominational support for theological schools as a percentage of the schools’ budgets has declined (although in many cases the actual dollar amounts have risen). And during the Great Recession, individual gifts also declined, although they have bounced back since then. Many seminaries have compensated by relying more heavily on tuition.

Increases in seminary tuition have outpaced inflation for the past two decades, and the problem continues to get worse. Debt loads are high and rising. But the need for well-prepared, well-educated Christian leaders is no less than before.

As a result, there’s frustration all around. Several years ago, the Christian Post quoted Don Davis of the Urban Ministry Institute expressing his own frustrationthis way: “The only way to get through seminary is to have wealth or know somebody rich. The working poor need not apply.”

When the pool of potential seminary students is made up of so many who are already carrying undergraduate and consumer debt, when the percentage of seminary costs borne by students is so high, and when the income potential for seminary graduates is so low, enrollment will be affected. We know that higher levels of undergraduate debt results in students seeking higher-paying jobs. Conversely, it is evident that students will lower levels of debt tend to focus on obtaining more meaningful positions, not just higher-paying ones.

Student loan debt can damage the success of graduates in their ministry roles

Fifteen years ago, the Auburn Center for the Study of Theological Education published a report on a comprehensive study it conducted called “The Gathering Storm: The Educational Debt of Theological Students” (www.auburnseminary.org/report/the-gathering-storm).

The Auburn study concluded that high levels of student debt have far-reaching effects on graduates in the following areas:

- Career choices

- Ability to purchase a home

- Saving for children’s education

- Saving for retirement

- Health care needs

- Stress levels in their personal and professional lives

Debt has even wider societal impacts as well. It is a contributing factor to delays in marrying, having children, buying homes, and starting businesses. Economists are beginning to attribute lower projected economic growth as a result.

One study shows that today, the average debt load for a seminarian who has borrowed to help pay for an M.Div. degree is $66,000. But are seminaries accomplishing their mission of preparing students for ministry, scholarship, and service if financial constraints prohibit their graduates from taking positions in these fields?

If not, what can seminaries do about it? While there are no easy answers, here are some strategies:

This is a simple way to reduce overall borrowing, but it is not easy. A school must have a substantial endowment or other funding vehicles to accomplish this. To do this, a seminary must embark on a long-term strategy that includes targeted fundraising and a focused strategy to build scholarship funds. A lot of donors must be found who believe in the long-term mission and viability of the institution and who are motivated to provide scholarships.

- Student financial planning

For most theology students, finance is neither a particular talent nor a fun hobby. When you combine the lack of skill and passion for the subject with a challenging and potentially distressed financial picture, dealing with finances can be drudgery.

Schools can respond to this by proactively providing student financial planning to help students reduce debt levels. Robust, personal financial planning can help relieve stress and put students and future church leaders on a path of more responsible and successful financial lives. Some schools have done this in house by utilizing the skills of someone who is already part of the administrative team. But it can also be done by developing relationships with local financial planners who might be willing to provide their services at a reasonable rate.

Financial planning helps students build and understand a current realistic budget to make sure they are not overborrowing. It also helps them project a postgraduation budget based on realistic assumptions of their future income and expenses.Having a plan in place often reduces financial anxiety.

A seminary can cease to participate in federal loan programs. This is a radical approach and the problems with it are obvious. For one, students may choose to enroll in institutions that participate in the federal loan program over those that do not. In addition, students who attend a school that doesn’t participate in a federal loan program may end up taking on more unsecured loans (like credit card debt), which typically carries higher interest rates than federal student loans.

Less drastic than cutting off access to loans altogether, schools can consider taking steps to slow the amount of debt their students incur. For example, they can require students to fill out additional forms or undergo mandatory counseling and financial education before participating in the federal loan program.

- Educational tracks for working students

Many theological schools create schedules that allow or even encourage students to hold full-time employment while they attend. We know that students who work full time borrow significantly less than those who do not.

- Screening applicants for financial viability

Schools can require prospective students to provide a complete financial picture when they apply. They can make sure they have a workable plan to finance their education. Do they already have significant debt? Are their assets or income too low to manage their current debt during their seminary years? If prospective students do not have a workable plan to address their existing financial burden, as well as any new debt that they may acquire while attending theological school, the school may deny or defer admission.

Conclusion

This is a difficult environment. Costs and debt levels are higher than ever. Graduates of theological schools are not promised a profession that will provide lucrative salaries and benefits. Seminaries must recognize the environment and find a strategy that will increase the overall pool of students who will graduate with healthy financial statements and fiscal habits that will support a lifetime of undistracted and fruitful ministry.